Nexo enables beginners and busy investors seeking bank-like simplicity to buy, earn, borrow, and spend all in one place. But what exactly is this platform serving over seven million users and processing over $370 billion? Why should you care? Nexo also states that it operates in over 150 jurisdictions and holds over $11B in assets.

This review strips jargon and focuses on real costs, typical yields, and the risks you face. We test the flows you use first on day one, then map card rewards and loyalty tiers. We also assess security, audits, and availability. By the end, you can judge if convenience outweighs tier rules, token exposure, and custodial risk – and if Nexo is for you.

What is Nexo?

Nexo is a Swiss-based cryptocurrency-focused wealth management platform founded in 2018. It reported over $11 billion in assets under management. The company, headquartered in Zug, was founded by Antoni Trenchev, Kosta Kantchev, and Kalin Metodiev. The founders previously built the consumer lending fintech Credissimo, which shaped Nexo’s operating playbook.

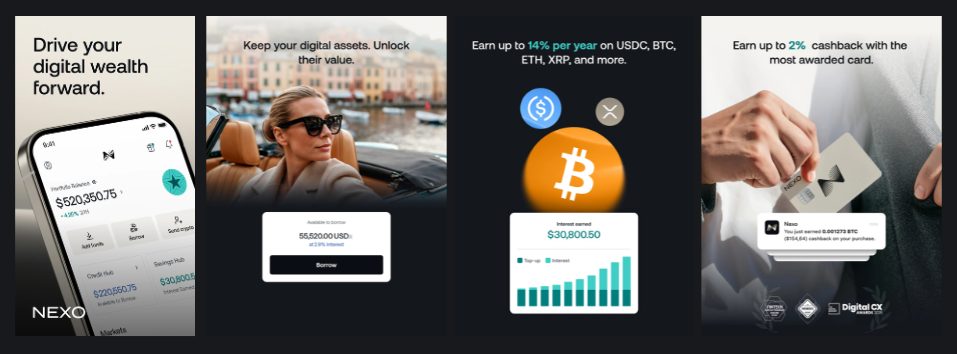

Nexo functions as a digital assets wealth platform, offering services such as earning interest, borrowing against crypto, trading, and spending with a single account. It combines Flexible and Fixed-term Savings with daily payouts and headline rates up to 14 percent, depending on asset and tier.

Borrowing starts from 2.9 percent annual interest via crypto-backed credit lines, so you can access liquidity without selling holdings. The Nexo Exchange supports 100+ assets, and Futures are available for experienced traders.

For comparison, this article lists the best crypto lending platforms to use in 2025.

On security and compliance, Nexo highlights institutional-grade custody and partnerships with firms such as Ledger, Fidelity Digital Assets, and Chainalysis. The company also offered real-time reserve attestations with Armanino in 2021 before audit firms reduced crypto work in 2023.

Nexo’s core products

In this section, we’ll walk you through each product so you know how the flows work, what fees apply, and what to expect.

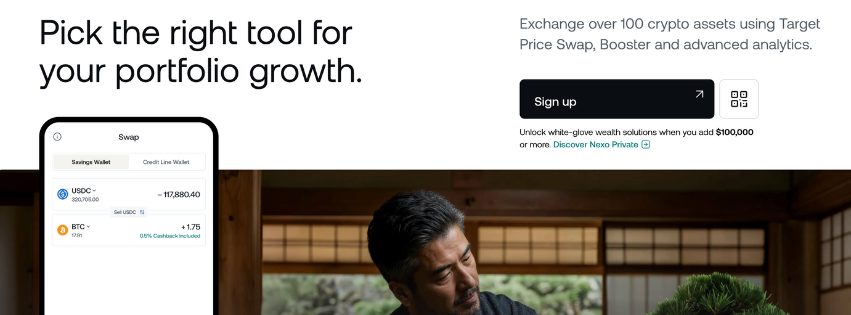

1. Buy/Sell & Instant Exchange

This is the beginner on-ramp inside the Nexo mobile app. You can fund with a bank transfer or a card, then swap between assets in a few taps. The process remains straightforward: select an asset, preview the quote, review any applicable fees or spreads, and confirm.

Card purchases settle fast but often cost more than bank funding. Instant swaps are convenient, yet the quote can include both a service fee and a buy/sell spread, especially during volatile periods. For larger amounts, sanity-check the price quality against Nexo Pro before executing.

Mind the rails you use. Some assets have network-specific deposit rules, so always match the network shown in-app before sending funds. Limits and regional availability apply, and they can change.

Start small. Make a test buy to learn funding times, settlement behavior, and how quotes move in busy markets. Once you’re comfortable, scale up with confidence.

2. Nexo Pro: spot trading and fee tiers

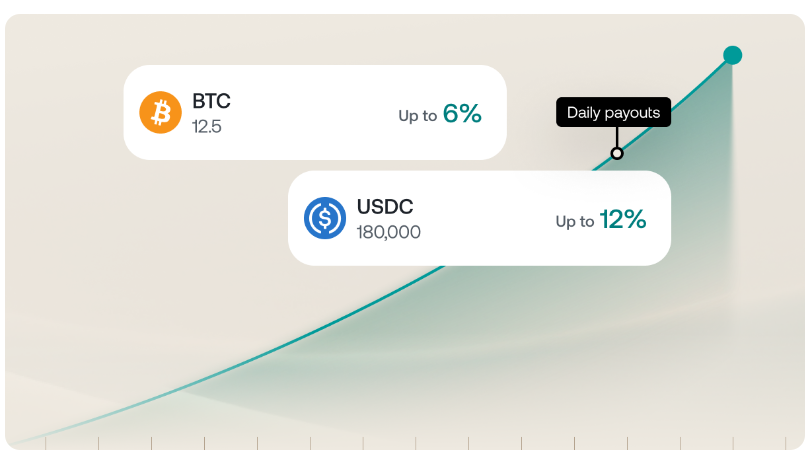

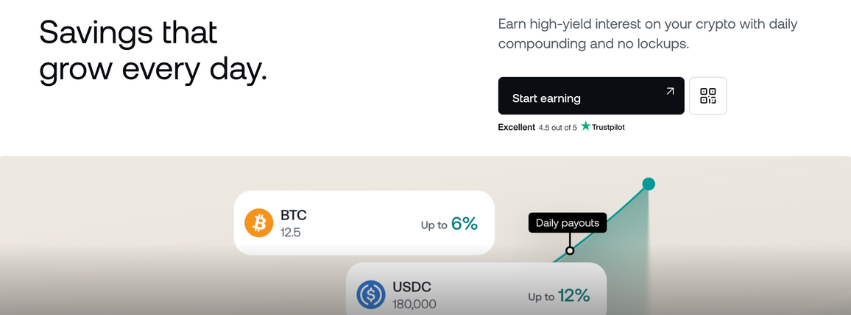

Earn pays interest on supported assets. Choose Flexible Savings for daily payouts and anytime withdrawals – a straightforward parking spot. Pick Fixed-Term Savings to lock funds for a set period in exchange for a higher potential rate. Your actual yield depends on the asset, the term, and Loyalty tier.

Watch the fine print. Some assets have balance caps or step-down rates above certain thresholds. While locked, funds usually can’t serve as collateral, vital if you also use a Crypto Credit Line.

Know how compounding works and how new rates apply to existing balances. Diversify across assets and terms to access cash without prematurely breaking a fixed position. If liquidity is your priority, favor Flexible and lock only what you can leave untouched.

3. Earn: Flexible vs. Fixed terms, caps, caveats

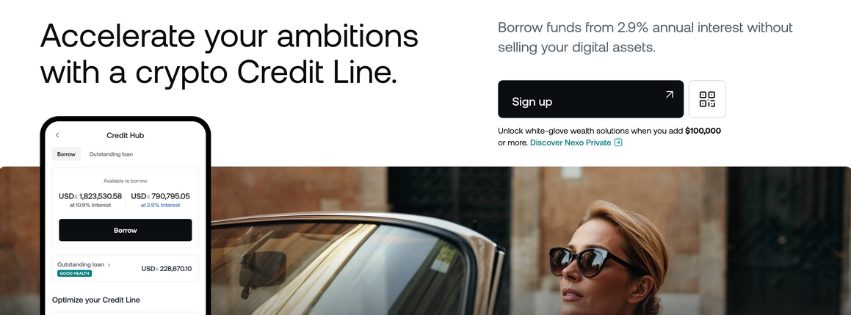

The Crypto Credit Line lets you borrow against your portfolio without selling. You pledge approved assets as collateral, draw cash or stablecoins, and repay on your schedule. Your loan-to-value (LTV) moves with the market, rising when prices fall, dropping when they rise. On Nexo, lower LTVs typically qualify for better lending rates in 2025.

Risk management is built in. If your LTV approaches the platform’s threshold, you’ll get alerts. At that point, add collateral, repay, or do both to bring LTV down. If you ignore the warnings, Nexo can sell a portion of your collateral to restore the ratio.

Costs track usage, not limits. Interest accrues daily only on the amount you’ve drawn, not on your full credit line.

Remember that collateral isn’t equal. Some assets are valued at a lower collateral factor, which reduces the amount you can borrow. Borrow conservatively, keep a cash buffer, and review auto-repay settings before you draw.

4. Lending and Borrowing: Crypto Credit Line

The Crypto Credit Line lets you borrow against your portfolio without selling. You pledge approved assets as collateral, draw cash or stablecoins, and repay on your schedule. LTV moves with the market, rising when prices fall and dropping when they rise. On Nexo in 2025, a lower LTV generally unlocks better lending rates.

Protection is built in. If your LTV nears the risk threshold, you’ll get alerts. Add collateral, repay, or do both to bring it down. Ignore the warnings and the platform may sell a portion of your collateral to restore the ratio.

You pay only for what you use. Interest accrues daily on the drawn balance, not on your full credit limit.

Remember that collateral weight varies. Some assets count less toward collateral value, reducing your ability to borrow. Borrow conservatively, keep a cash buffer, and review auto-repay settings before you draw.

5. Nexo Booster

Booster allows you to increase exposure to a coin without adding new funds. You use existing holdings as collateral, Nexo extends a crypto credit, and the system auto-buys the target asset in one flow.

Nexo describes a permitted LTV of up to 70% on Booster and typical exposure ranges of roughly 1.25x to 3x. You pay your normal borrowing APR on the drawn amount plus any trading spread. And your LTV will rise faster if prices drop because you are holding more of the asset. Many regions limit leverage, and some assets carry different collateral factors.

Start with a small size and keep a buffer so routine volatility does not push you toward liquidation. Example: boost $1,000 in BTC to about 2x exposure. A 20% price drop raises LTV quickly, so plan for top-ups or partial repayment.

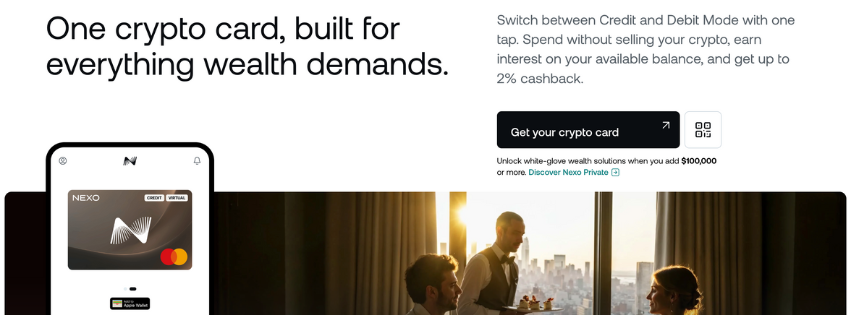

6. Nexo Card: Credit Mode vs. Debit Mode, cashback rules

The Nexo Card links your crypto account to everyday spending, working in two ways. Debit Mode allows for direct spending from your balances, providing clean, predictable outflows. Credit Mode borrows against your collateral, preserving your long-term positions and, on eligible purchases, earning tier-based Nexo Card cashback.

Rewards aren’t one-size-fits-all. Cashback rates depend on your Loyalty tier and the reward currency you choose. Some merchant categories and cash-like transactions, such as prepaid loads or gift cards, don’t qualify. Foreign-exchange fees and ATM allowances also vary by country, tier, and time period.

Select the mode that best matches your intent. Use Debit Mode when you’re budgeting tightly and want straightforward costs. Switch to Credit Mode when you prefer to maintain exposure to your assets and can effectively manage the borrowing dynamics.

Before you tap, confirm in-app eligibility, as card availability varies by country. If you’re traveling, review local FX rules and your monthly ATM limits. Then track rewards in the app to see which purchases earned cashback and which were excluded.

7. Futures: leverage, margin, and risk controls

Futures introduce leverage, which magnifies both gains and losses. On Nexo Futures you trade from a dedicated Futures Wallet with cross margin, and a margin-risk meter that climbs as exposure increases.

Perpetual contracts never expire; instead, funding payments flow between longs and shorts at set intervals. You choose leverage within platform caps, blue-chip pairs usually allow more than thinly traded markets. If the risk meter crosses key thresholds, you’ll receive warnings; forced position reduction or liquidation can follow.

Start small and observe how funding affects P&L over a full day. Set price alerts at your decision levels. Keep surplus collateral in the Futures Wallet so normal volatility doesn’t trigger avoidable liquidations.

If you’re new, treat leverage as a tool for specific setups, not the default setting. New traders should start small and learn the mechanics of perpetual futures trading first.

8. Loyalty Program: Base, Silver, Gold, Platinum

Nexo loyalty tiers are based on how much NEXO you hold as a share of your portfolio. As you move up, you can boost Earn APYs, cut borrow APRs, raise card cashback, and increase fee-free withdrawals.

To qualify, you must meet both the minimum account balance requirement and the NEXO percentage for each tier. But perks aren’t uniform. Benefits vary by asset and product, and many boosts apply only up to set caps. Holding more NEXO also increases your token exposure to overall risk.

Choose the tier for your goal, not the badge. If you borrow, model your APR at two tiers and weigh the extra NEXO you’d need to hold. If you chase yield, check the actual APY increase on the specific assets you’ll hold.

Writer’s note: Nexo crypto interest rates and daily payouts are available in Flexible and Fixed-term Savings. Nexo lending rates and LTV are tied to the Credit Line. Nexo card cashback depends on Loyalty tiers. The question of Nexo’s safety and legitimacy in 2025 relates to custody and compliance, which are covered elsewhere in this review.

9. Nexo Business

Nexo offers Business bundles that encompass multiple institutional services within a single framework.

Corporate Accounts let companies or family offices park and manage digital assets separately from personal holdings. A Prime Brokerage interface aggregates liquidity, trading, and lending so larger investors do not need multiple venues.

For firms building their own front-end, Nexo’s White Label option rebrands its custody, exchange, and credit rails. Early-stage teams can also tap Nexo Ventures for equity or token funding alongside operational advice.

Finally, an integrated Payment Gateway enables merchants to accept settlement in major cryptocurrencies, routing transactions through Nexo’s custody layer.

Together these products present a modular toolkit rather than a single-path offering, leaving organisations free to adopt only what fits existing workflows without extra vendor lock-in risk.

Nexo supported countries

| Region or Country | Core access | Nexo Card | Nexo Pro |

| European Economic Area (EEA) | Generally available, the asset list varies | Available to EEA residents | Available in EEA, per product terms |

| United Kingdom | Generally available, product mix varies | Available to UK residents | Nexo Pro is unavailable to UK residents |

| United States | Re-entered the market in Apr 2025 | [Confirm on app] | [Confirm on app] |

| Australia | Margin trading is currently unavailable | [Confirm on app] | Margin trading currently unavailable |

| Global (other) | Many countries supported | [Confirm on app] | [Confirm on app] |

Updated fees & rates

Below, we break down Nexo’s trading fees and costs, each with a quick dollar example. And you’ll learn where costs are hidden, how tiers affect pricing, and which path is the most cost-effective for your next trade or transfer.

Nexo Pro trading fees

What it means: Nexo’s fee schedule confirms that fees are tiered based on 30-day trading volume but paying fees with the NEXO Token cuts them in half. For context, Maker orders add liquidity while taker orders hit existing quotes.

| Fee type | Typical cost/range | Example | Key rules |

| Maker/Taker fees | Maker 0.04%–0.20%. Taker 0.07%–0.20% | $1,000 taker trade at 0.20% = $2 | 30-day volume sets tier. Pay fees with NEXO to halve the fee |

Exchange spreads and instant swaps

The “Swap” feature in Wallet can include a spread, which is the gap between the buy and sell prices. Nexo charges a 0.75% transaction fee for its in-wallet swap service. For price-sensitive trades, compare the Swap quote to Nexo Pro’s order book.

| Fee type | What it covers | Typical cost/range | Example |

| Swap fee + spread | In-wallet “Swap” quotes | 0.75% service fee + embedded spread | $1,000 Swap at 0.75% = $7.50 (+ any spread) |

Borrow APRs and LTV effects

What it means: Credit Lines are secured by your crypto. Your loan-to-value (LTV) moves with prices. Lower LTVs qualify for lower APRs. If LTV rises, rates step up and liquidation risk increases.

| Credit type | What it covers | Typical cost/range | Example |

| Crypto Credit Line APR | Interest on drawn balance | From 2.9% APR at Platinum when LTV < 20% | $10,000 at 2.9% ≈ $290/yr or $0.79/day |

Note: Nexo’s low-cost credit lines offer APRs as low as 2.9% for Platinum Loyalty Tier clients, but this is contingent on the Loan-to-Value (LTV) ratio remaining below 20%.

Earn APYs

Nexo offers both flexible and fixed-term savings options. Flexible Savings pays daily and lets you withdraw anytime. Fixed-term Savings locks funds for higher “up to” rates. Your Loyalty tier, asset, and term drive the effective yield you actually get.

| Earn feature | What it covers | Typical yield | $ example |

| Flexible vs Fixed | Interest on supported assets | Flexible up to 14% APY. Fixed up to 15% APY | At 14% APY, $1,000 ≈ $140/yr |

Card fees, FX, ATM, and cashback

Nexo’s card operates in both “Credit Mode” (using a crypto-backed line of credit) and “Debit Mode” (spending from your available balance). FX fees depend on location and day. Cashback depends on the Loyalty tier. Always check in-app eligibility.

| Type | What it covers | Typical cost/range | Example |

| FX fees | Purchases in foreign currency | Weekdays: EEA/UK/CH 0.2%, ROW 2%. Weekends: EEA/UK/CH 0.7%, ROW 2.5% | $200 EEA weekday purchase at 0.2% = $0.40 |

| Cashback | Rewards on eligible card spends | Up to 2% in NEXO or 0.5% in BTC at Platinum | $100 eligible purchase at 2% = $2 in NEXO |

| ATM | Cash withdrawals | Tier-based free allowance, then fee applies | — |

Network and withdrawal fees

Nexo covers many blockchain withdrawal fees for Loyalty members and shows the live network quote before you confirm. Bank withdrawals have tier-based allowances. This is where Nexo’s fee-free withdrawals matter most.

| Item | What it covers | Typical cost/range | $ example | Key rules |

| Crypto withdrawals | On-chain transfers | “Unlimited free withdrawals on 15+ networks” for eligible tiers; else network fee shown in app | Within allowance on supported networks = $0 | After allowances or unsupported networks, you pay the live blockchain fee |

| Bank withdrawals | Fiat to bank | One free per month for eligible tiers, then fee | First monthly bank withdrawal = $0 | Allowances vary by tier; follow in-app steps to avoid delays |

Safety, custody & regulation

Nexo uses institutional-grade custody and undergoes independent audits, operating at scale across more than 150 jurisdictions. We focus on how your assets are stored, who audits the controls, and where Nexo can serve you.

It relies on third-party custodians such as Ledger Vault and Fireblocks rather than holding your coins on an exchange hot wallet. Independent SOC 2 and SOC 3 audits validate key security controls annually.

Nexo previously offered real-time “proof of reserves” attestation through Armanino in 2021. The industry’s approach has shifted, so treat proof-of-reserves as an evolving control and weigh it alongside audits and custody details.

Custody model and insurance at the custodian level

Nexo custody relies on specialist providers rather than a single exchange hot wallet. Partners like Ledger Vault and Fireblocks implement multi-sig approvals, segregated accounts, and hardware security modules so no single keyholder can move funds.

Insurance sits at the custodian, not the user level. It’s crime insurance designed for specific theft events and governed by policy terms, limits, and exclusions. It isn’t FDIC or SIPC coverage, and it isn’t per-customer protection.

You still control the movement of your assets. Use withdrawal allowlists and device approvals, and transfer off-platform any time, subject to network conditions and your tier allowances. Treat insurance as one layer; also weigh the custody architecture, access controls, and incident-response practices.

SOC 2 and SOC 3 audits, certifications, and attestations

SOC reports tell you how a platform runs, not how it’s financed. A SOC 2 Type 2 test security and related controls over a defined period; SOC 3 is the shorter, public version you can read without an NDA. Together, they shed light on access management, change control, monitoring, and incident response.

But they aren’t financial audits, and they don’t measure solvency. When they’re available, also read any reserve attestations or custody-process reports, and note both the issuance date and the scope; they determine what was actually examined.

Then zoom out. Pair the audit evidence with custody architecture and regional licensing before deciding how much to keep on-platform. For scale context, Nexo says it has paid over $1.2B in interest since 2019 and processed more than $371B in transactions and collateralized credit since 2018.

Infrastructure service providers and operational resilience

Behind the app, Nexo relies on a network of third-party providers: custodians for key storage, settlement partners for fiat rails, analytics tools like Chainalysis for on-chain monitoring, and identity vendors for KYC.

This separation of duties reduces single-point risk and allows upgrades without service interruption. You benefit from features like address allowlists, withdrawal reviews, device management, and real-time risk flags that ride on these vendors’ APIs.

And because providers operate under their own certifications and controls, you can review their public documentation as part of your due diligence. If a vendor incident occurs, operations can be rerouted or paused while protections remain in place.

Licenses, registrations, and product eligibility by region

Nexo operates through local entities and registrations where required, with product availability set by jurisdiction. Card access currently centers on EEA and UK residents, while features like Earn and Futures can vary by country and change as rules evolve.

You will confirm eligibility in-app during onboarding and again at the product level before funding. Expect full KYC, AML screening, and sanctions checks as part of compliance.

If you plan to travel or relocate, review your region’s terms, withdrawal allowances, and card FX rules in advance. When in doubt, consult the Help Center pages for the latest list of supported countries and restricted jurisdictions.

The Nexo App

Nexo’s app is built to make it feel familiar if you’ve used online banking. You sign up, verify your identity, add funds, and then buy, earn, borrow, or spend from one dashboard. For context, Nexo has stated it serves over 7 million users across more than 150 jurisdictions and has processed over $130 billion in digital-asset transactions.

This section focuses on the Nexo user experience mobile app from a beginner’s point of view, so you know what happens on day one and what to expect next.

Account setup, KYC, funding options: Step-by-step

Create your account

Download the app or use the web platform, add your email, set a strong password, and enable two-factor authentication. You’ll finish in minutes.

Complete KYC

Provide basic details, scan a government ID, and take a selfie. Nexo explains why it collects this data and how it stores it. And some users may be asked for a document with their address.

Choose a funding path

Bank transfer: Add funds in your name for USD, EUR, or GBP and follow the in-app instructions for SWIFT, SEPA, or Faster Payments where supported. Bank funding reduces card fees and suits larger amounts.

Card buy: Purchase instantly with Visa or Mastercard, including Apple Pay or Google Pay. It’s fast for small amounts, though the quote may include a spread or fee.

Crypto deposit: Copy your asset’s deposit address and network from Nexo, send from your external wallet or exchange, and wait for blockchain confirmations. But always match the network.

Withdrawals when needed

Send crypto out using the same asset and network rules, or withdraw fiat to your bank from your USD, EUR, or GBP balances. Follow the on-screen steps to avoid delays.

App and dashboard

Start by checking your total balance and individual assets, then tap ‘Buy’ or ‘Swap’ to make a small test trade. Enable Earn on supported assets, explore the Card tab, and review Rates and Fees before scaling up.

Support, responsiveness, and help center

You get 24/7 Client Care via live chat, email, and a web form. The Help Center covers onboarding, bank transfers, crypto top-ups, and troubleshooting with clear step guides. And you can escalate from any article if needed.

Where Nexo is and isn’t available

- Global footprint: Present in over 150 jurisdictions; availability varies by product.

- Nexo Card: Available to citizens and residents of selected European countries, including the EEA and the UK.

- United States: Paid $45 million in January 2023 to settle with the SEC and states over its Earn Interest Product, then announced a U.S. re-entry on April 28, 2025. Check the app for the live product set.

- Restricted jurisdictions: Before funding, see Nexo’s Help Center list. Rules change, and individual products may differ.

What new services did Nexo launch in 2025?

In 2025, Nexo introduced several upgrades, some of which are already available to users, while others are still being rolled out.

This overview will provide a beginner-friendly look at these updates, connecting each one to practical choices you can make.

We will also explore how these developments relate to Nexo’s global expansion, security features, and safer trading practices.

Nexo perpetual futures: Use cases and core risks

Perpetual futures let you trade with leverage and no expiry. Use them to hedge spot, express short-term views, or fine-tune risk without touching long-term holdings. On Nexo, you can trade from a dedicated Futures Wallet with cross margin, so one collateral pool backs all open positions.

You’re allowed to pick leverage within preset caps; larger coins typically allow more than small caps. A margin-risk meter tracks exposure and triggers warnings at key levels. If risk continues to rise, the platform can reduce positions or liquidate. Funding payments flow between longs and shorts to keep prices near spot, sometimes helping your P&L, sometimes hurting it.

Start with small size, set price alerts, and keep extra collateral in the Futures Wallet. Many regions restrict leverage. Check your eligibility, fees, and current funding before the first order.

Nexo Card: Credit vs Debit Modes and Cashback basics

The Nexo Card links your account to everyday spending and lets you switch modes in-app. Credit Mode borrows against your collateral and pays tier-based cashback on eligible purchases. Interest accrues only on what you draw, not your full line. Debit Mode spends directly from balances and doesn’t create a loan.

Cashback rates depend on your Loyalty tier and chosen reward currency, and some merchant types or cash-like transactions don’t qualify. FX fees and ATM allowances vary by region and sometimes by day.

Availability also differs by country. Before you rely on the card, confirm in-app eligibility, local FX rules, and your current tier limits. After each purchase, check the rewards log so you know what earned and what didn’t.

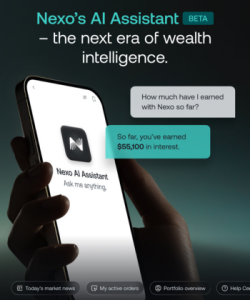

Nexo AI Assistant

Nexo’s AI assistant lives inside the app and answers simple account and market questions in plain English. You can ask about yesterday’s interest, your current LTV, upcoming card perks by Loyalty tier, or what “funding” means in Futures.

It pulls from your account data, live market feeds, and Help Center articles, then explains the next step you could take. And it maintains the beginner-friendly flow by linking directly to the action you need, such as enabling Earn or transferring funds to reduce LTV.

Availability may vary by region, and the assistant provides informational support, not investment advice. You can review what it shows and act only when you’re ready.

Try prompts like “How much interest did I earn last week,” “What is my LTV and buffer,” or “Explain BTC perpetual funding today.” It shortens the learning curve without changing your risk controls.

Audit status: SOC 2 and SOC 3 reports

On August 1, 2025, Nexo says it completed SOC 2 Type 2 and SOC 3 Type 2 audits with A-LIGN in August 2025. Think of SOC 2 Type 2 as an independent test of security and related controls over a defined period; SOC 3 is a shorter, public summary.

These attestations examine areas like access management, change control, and incident response. They don’t value assets, prove solvency, replace proof-of-reserves, or eliminate counterparty risk.

Use them to compare Nexo’s control maturity with peers, not as a blanket safety guarantee.

If your question is whether Nexo is safe and legit in 2025, pair the SOC reports with details on custody setup, any insurance at the custodian level, and the rules in your jurisdiction. Then decide how much you’re comfortable keeping on-platform.

The Nexo token

$NEXO is Nexo’s native utility token, launched in 2018 to power loyalty tiers and platform perks.

It underpins Nexo loyalty tiers’ benefits by linking your portfolio’s NEXO share to higher Earn APYs, lower borrow APRs, fee discounts, and card cashback. Nexo has also run buyback programs, and in 2021, it proposed moving from occasional dividends to daily interest via governance. These mechanics define the token’s core utility rather than pure speculation.

For a quick financial snapshot, CoinMarketCap reports a circulating supply near 646.1 million NEXO, a 1.0 billion max supply, and a market cap of close to a billion ($800M). These figures can help you compare utility tokens across exchanges and lending apps.

Nexo Anti-Scam engine: Real-time, risk-based client protection

Nexo has rolled out a default Anti-Scam Engine that monitors transactions in real-time and intervenes only when risk increases. The system blends contextual analysis, blockchain security integrations, and multiple intelligence feeds to spot subtle red flags.

You’ll see short, explainable prompts with clear choices to review or proceed; in rare high-risk cases, Nexo briefly pauses the transfer for rapid internal review to prevent losses. The design aims to avoid blunt overblocking while acting decisively when behavioral or transactional signals suggest danger.

It targets scams that hit users hardest, including romance grooming, tech-support impersonation, and high-yield Ponzi-style schemes. Chainalysis estimates crypto scams siphoned at least $9.9 billion in 2024, underscoring the need for prevention.

The engine is live on Ethereum, Optimism, BNB Chain, Polygon, Arbitrum, Avalanche, and Base, with phased expansion to Bitcoin, Solana, Tron, and XRP. As intelligence updates, protections adapt, so you stay protected without unnecessary friction.

Nexo’s pros and cons

Nexo suits beginners who want one app to earn, borrow, trade, and spend, with clear rates and daily payout interest. Below, we weigh the practical benefits against the trade-offs to understand how the platform compares to other options.

What Nexo does well

- Clean onboarding and one dashboard in the Nexo user experience mobile app

- Daily payouts on Flexible Savings; higher APY on Fixed terms

- Borrow without selling; low rates at lower LTVs

- Dual-mode card with tiered Nexo card cashback

- Maker–taker fees on Nexo Pro; clear pricing, fee discounts with NEXO

- Tier-based free crypto withdrawals and bank allowances

- Third-party custody plus recent SOC 2/SOC 3 audits support Nexo security features

Where it lags/trades off

- Card availability is still uneven beyond the EEA and the UK

- Holding NEXO for Nexo loyalty tiers benefits adds token price risk

- Instant swaps can carry spreads; Pro usually prices tighter

- Custodial counterparty risk remains even with audits

- Liquidations can hit fast when LTV spikes

- Ongoing Nexo proof of reserves concerns for users who want real-time checks

Nexo’s growth plans/roadmap for 2025

- U.S. re-entry confirmed as completed on April 28, 2025.

- Nexo Card goes global (new markets, cashback in Debit Mode, subscription rebates, brand campaigns) ~ Expected: Q4, 2025.

- Resume physical Nexo Card orders ~ Status/Expected: Paused Jan 17, 2025; “working on resuming,” date not provided.

- New NEXO Token utilities (Launchpool, revamped Loyalty Program, dust-to-NEXO, new exchange listings) ~ Expected: 2025, month not specified.

- AI-powered features (automated portfolio management, AI assistant) ~ Expected: 2025, month not specified; AI insights highlighted Mar 19, 2025.

- Trading upgrades

- 100x leverage contracts / structured products ~ Launched: Aug 2025.

- Multi-asset collateral for Futures; automated OTC ~ Expected: 2025, month not specified.

- Expanded core offering (longer fixed terms; Private clients’ auto-repayment limit) ~ Expected: 2025, month not specified.

- Business products (White-Label solution, Payments Gateway, enhanced corporate onboarding) ~ Expected: 2025, month not specified.

- Cross-border transfers (new account funding options, third-party payments framework) ~ Expected: 2025, month not specified; payments in USD, EUR, GBP noted Mar 19, 2025.

- Brand and awareness (global brand campaign, sports sponsorships, expanded language support, welcome rewards) ~ Expected: 2025, month not specified.

- Policy and product updates (EEA stablecoin services) ~ Effective: Mar 10 and Mar 31, 2025 (two phases).

Conclusion

Verdict: Nexo is a strong pick if you want one app to buy, earn, borrow, and spend without a heavy setup, and here’s why.

Onboarding is straightforward. You earn daily interest on flexible balances, and you can lock funds for higher fixed rates when you don’t need liquidity. If you borrow, the crypto credit line works, provided you monitor LTV and top up during dips.

The card adds utility where it’s supported, while Nexo Pro suits active traders who want more transparent pricing. Security controls and third-party audits help, yet they don’t erase platform or token risk. The loyalty tiers are evident in fees and yields; perks increase as you hold NEXO and maintain larger balances.

Choose Nexo if convenience and integrated features matter most today. Look elsewhere if you need broad card availability, continuous proof of reserves, or self-custody by default.

FAQs

Is my crypto “insured” on Nexo?

Is Nexo regulated?

Can U.S. users access Earn and the Card today?

How does card cashback actually work?

What happens if my collateral drops?

References

Crypto firm Nexo Capital agrees to pay $45 mln to settle US SEC, state charges | Reuters

At event with Donald Trump Jr in Bulgaria, crypto firm Nexo announces U.S. return | Reuters

Digital Asset Platform Nexo to Return to U.S., Cites Crypto Optimism | CoinDesk