One of the biggest advantages of micro-investing is that it’s accessible to everyone. You can start investing with £100 or even just a few pounds on many platforms and apps. This makes investing easier and lets people from all backgrounds participate in the financial markets. Regular investing is a proven strategy for building wealth.

The National Study of Millionaires, published by Ramsey Solutions in April 2020, showed that three of four millionaires attribute their success to regular, consistent investing over a long period. The number of people in the UK who regularly invest is growing. A survey by Censuswide showed that in 2025, an estimated 29 million Brits (54%) have invested, an increase from 51% in 2024.

If you’re considering joining the trend, our guide will provide a solid starting point. Read on for a summary of the best options for investing a little money each month and reviews of several brokers to invest with:

An overview of the top methods to invest £100 a month in the UK now

The beauty of just investing £100 a month is that nearly anyone can afford to put aside that much every month, and once you make a habit of it, the money that’s invested will benefit from compounding interest. There are eight effective ways to invest £100 a month:

- Index Funds: These funds track a market index, such as the S&P 500, offering diversification and generally low fees.

- Exchange-Traded Funds (ETFs): Similar to index funds, ETFs provide diversification but often have more flexibility in terms of asset classes.

- Target-Date Funds: These funds automatically adjust their asset allocation over time to align with your retirement date, making them a hands-off investment option.

- Individual Stocks: If you have the time and knowledge, investing in individual stocks can offer the potential for higher returns. However, this also comes with increased risk.

- Bonds: Bonds offer a relatively stable return, but they have less growth potential compared to stocks. Staples of income investing.

- Real Estate Investment Trusts (REITs): REITs allow you to invest in real estate without owning physical property.

- Robo-Advisors: These automated investment platforms use algorithms to create personalised portfolios tailored to your risk tolerance and financial goals.

- Savings Accounts: While not technically an investment, high-yield savings accounts can offer a safe place to grow your money.

- Show Full Guide

A closer look at the ways you can put £100 a month to work to build wealth

These financial instruments all have certain advantages for investors seeking to invest a small amount of money each month. The key to all of them is that they can enhance the diversification of a portfolio and simplify investment decisions.

Index funds

Index funds are a type of mutual fund that tracks a specific market index, such as the S&P 500 or the Nasdaq Composite. Instead of trying to outperform the market by picking individual stocks, index funds aim to match the performance of the index they follow.

Some of the benefits of index funds include diversification, as they offer the opportunity to invest in a wide range of stocks, lower expense ratios compared to actively managed funds, and, over the long term, index funds have consistently outperformed actively managed funds.

In the short term, index funds aim to match the market’s performance, so they may not outperform it significantly. It’s relatively simple and easy to invest £100 a month in an index fund, though more experienced investors like to have a greater degree of control over their investments.

Pros

- Low-cost investing

- Diversification is easy with index funds

- Passive investing

Cons

- Lack of customisation

- Lack of control

ETFs

These investment vehicles pool money from investors to invest in a diverse array of securities, including stocks, bonds, and commodities. They generally have less expensive fees than mutual funds and can be more tax-efficient, especially when it comes to capital gains taxes.

They are highly liquid and trade like stocks, as they can be bought and sold throughout the trading day. Like index funds, they offer investors a way to diversify their portfolios. Some ETFs, however, may not perfectly track their underlying index, resulting in a tracking error.

Pros

- Low fees

- Tax efficient investing

- Transparency

Cons

- Some ETFs have tracking errors

- Market risks

Target-date funds

They are a type of mutual fund designed to provide a balanced investment portfolio that gradually becomes more conservative as you approach your retirement age. They’re designed for investors who want a hands-off approach to retirement saving.

They automatically adjust their asset allocation over time based on your target retirement date, gradually shifting away from riskier assets such as stocks to safer investments, like bonds. They are usually professionally managed, but this also means that they sometimes have high expense ratios.

Pros

- Ideal for passive investing

- Built-in diversification

- Help with risk management

Cons

- Limited customisation

- Some have high expense ratios/li>

Individual stocks

Investing in stocks, if you have the time to conduct thorough analysis, can be more lucrative than any other type of investment, with a better opportunity for growth. Even if you’re investing £100 a month, you can build up quite a nest egg by regularly investing.

While not all stocks are under £100, the growth of fractional shares will allow you to regularly invest in more expensive stocks and benefit from their share growth. Investing in stocks, however, carries more risk than some other types of investments and requires closer monitoring.

Pros

- Ability to customise investments

- Greater potential for growing wealth

- Some stocks provide share and dividend growth

Cons

- Can make it harder to diversify your portfolio

- Greater risk of losses

Bonds

They are essentially loans that you make to a government or corporation. In exchange for lending your money, you receive regular interest payments and the principal back at maturity. Bonds are generally considered a safer investment than stocks, but they also offer lower potential returns.

They can help diversify your portfolio, the interest earned on bonds can be tax-efficient, and they provide stable income, but often lower returns. If inflation rises faster than the interest rate on your bond, the purchasing power of your investment may decline. In some cases, the issuer of a bond can default, so there is some credit risk, depending on the type of bond you purchase.

Pros

- Stable income source

- Relatively low risk

- Help diversify your portfolio

Cons

- Lower returns

- Can be hurt by inflation

- Credit risks

REITs

They are companies that own or operate income-producing real estate properties. They collect rental income from properties such as apartments, office buildings, shopping centres, and industrial facilities.

REITs are required to distribute at least 90% of their taxable income to shareholders as dividends. As a result, they are recognized for paying above-average dividends and are favored by income-oriented investors.

REITs can provide diversification to portfolios, particularly if they hold a diverse range of real estate assets. REITs are vulnerable to market conditions, though, and when interest rates rose in recent years, many REITs struggled. Many REITS trade on regular exchanges, as if they were stocks. Some trade privately.

Pros

- Diversified exposure to real estate investing/li>

- Professional management

- Good liquidity

Cons

- Property risk

- Interest rate risks

Robo-Advisors

They are digital investment platforms that use technology to manage your money. After answering questions about your goals and risk tolerance, a robo-advisor will invest your funds in pre-made portfolios of ETFs. These platforms are ideal for beginners or those who lack the time to monitor the market.

One of the biggest benefits of robo-advisors is their low fees. Because they use technology instead of human advisors, they can offer lower costs. The biggest concern about robo-advisors is the lack of management. They utilise algorithms, and if they are flawed, that will hurt your investment.

Pros

- Low-cost investing

- Built-in diversification

- Good for passive investors/li>

Cons

- Little customisation

- Lack of personal touch

- Market risks

Savings accounts

When people think of savings accounts, they typically think of banks, but there are also numerous investment platforms that pay interest on uninvested funds. The beauty of savings accounts is that they are low risk and, as long as inflation isn’t high, are a guaranteed way to increase income.

It’s easy to regularly invest in savings accounts, and many online banks and stock platforms, competing for business, have raised their interest rates.

Pros

- Safe, little risk

- Easy to do/li>

- Easy solution to parking funds

Cons

- Low yields compared to other investments

- Limited growth potential

- Market risks

Why you should invest £100 a month in the UK

The reason for investing regularly, even as little as £100 a month, is obvious. If you had started investing just £100 in the S&P 500 in 2000 and added £100 regularly each month, your investment by 2025 would be worth between £175,000 and £180,000 – nearly triple the return of the same contributions to a savings account.

According to a recent white paper by BlackRock, the UK has seen the largest increase in investors, 21%, across 14 European markets since 2022. Those 3.5 million new investors belie the fact that nearly 62% of people in the UK do not invest.

The study further notes that 93% of regular investors are more likely to be confident in their long-term financial security. The key is regular investing, and roughly 37% of those in the UK who invest, or 4.3 million, do so with regular contributions, usually on a monthly basis. On average, current UK investors put aside £344 in an investment account or stocks and shares ISA.

Where to invest your £100 a month in the UK?

These eight platforms stand out for investing £100 a month:

1. eToro: Good for experienced investors

The platform, renowned for its user-friendly features and copy trading, offers more than 700 ETFs and more than 6,000 stocks across 20 global exchanges. For novice investors, ETFs are a good option for regular monthly investments of £100 due to their built-in diversification.

eToro also offers trades in forex, cryptocurrency, indices, commodities, and varied CFD (contracts for difference) trading. The platform also offers fractional shares, allowing investors to spread their investments across £100 a month. A fractional share is a part of one share of a stock or an ETF.

If the price of a stock is £100 and you invest £10, you would then own a fraction (1/10th) of that single stock. At eToro, you can buy fractional shares of stocks and ETFs of any size above its £10 investment minimum.

While eToro pays up to 4.3% interest on uninvested cash, this is reserved for traders with an uninvested balance over $50,000. Below that, it pays 3.5% interest on uninvested funds.

eToro does have decent educational resources, including its eToro Academy. This is useful as the onus is on investors to do their own research if they use the platform for investing £100 a month. It does have an option for recurring investing that allows you to invest for as little as $25 a month.

The broker also has Smart Portfolios that offer professionally managed portfolios that can help those looking to invest in specific market segments in a largely automated way. Find out more about our views on this broker from our eToro review.

Your capital is at risk.

2. XTB: Good educational assistance, high interest paid

The platform, based in Poland, offers a beginner-friendly way to invest £100 a month through its Intuitive Interface, which provides access to more than 1,800 ETFs for trading.

The service enables investors to create their own personalised plan, utilising specified amounts that will be automatically allocated across their portfolio’s funds, which can be tailored to match their risk tolerance and sector preferences.

The minimum investment amount is £10. There’s no commission on Intuitive Interface for monthly turnovers of up to £100,000. However, if you invest in foreign ETFs, a 0.5% currency conversion fee may apply. Once the Intuitive Interface is established, it will automatically allocate funds based on the specified percentages you select. The platform also offers more than 3,600 stocks for trading.

XTB’s also has an auto-invest feature that allows you to choose funds from your XTB account or set up recurring bank transfers to fund your investments, using the XTB app. It allows up to 10 personalised portfolios, each holding a maximum of nine ETFs.

XTB offers robust educational assistance, starting with a news feed that lists upcoming dividend announcements, a calendar of economic news, and a market sentiment indicator, as well as over 1,000 articles and videos. XTB will pay up to 4.25% interest on uninvested funds held in the account. If you don’t make any trades for a year, you will begin paying an inactivity fee of €10 a month.

73% of retail investor accounts lose money when trading CFDs with this provider.

3. Admiral Markets: Plenty of low-cost trading options

The London-based company, part of Estonia’s Admirals Group, makes investing £100 a month easy for individuals. It offers trading on more than 2,900 stocks and more than 350 ETFs. The minimum deposit is €250.

It also offers fractional trading on more than 700 stocks and ETFs, allowing investors to own a piece of a stock or an ETF for as little as €1. Admiral Markets also has an auto-investing option. You can create an auto-Invest plan using any stock or ETF offered by Admiral Markets.

It doesn’t charge a commission on direct share buying (though it benefits from the spread), and it offers more than 4,100 stocks for direct share buying.

You can set up recurring investments weekly or monthly through Admiral Markets’ Auto-Invest plan, and you can have as many as five Auto-Invest plans on one account. It has a monthly inactivity fee of €10 after two years of inactivity, and it charges a minimum of €250 to open an account.

If you’re looking for information on what to invest in, Admirals offers a wealth of resources, including webinars, articles, tutorials, guides, e-books, online courses, and even a glossary of terms. Check out our review of the broker, as well.

4. FP Markets: Good for experienced and novice investors

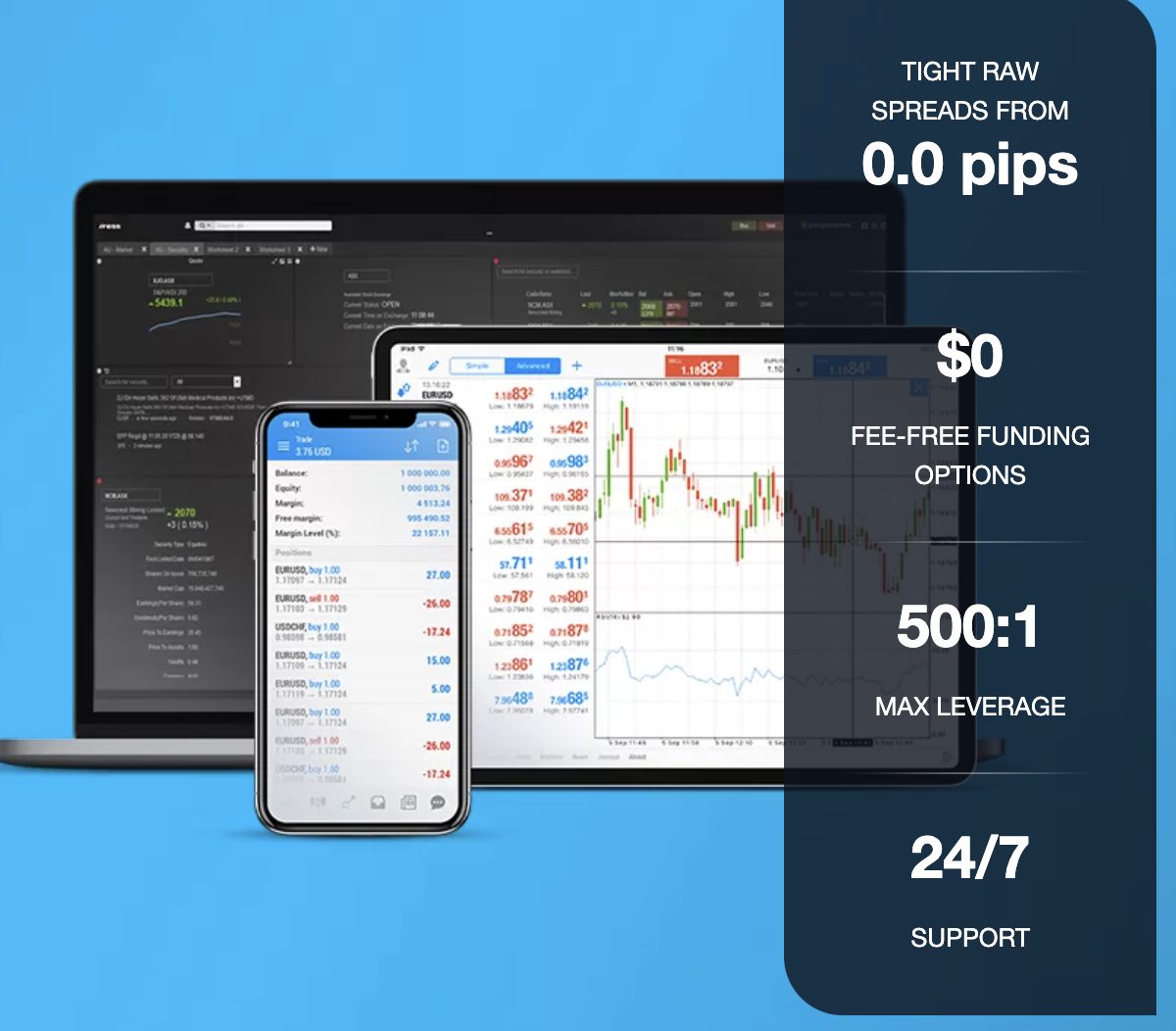

Launched in 2005, FP Markets is a multi-asset CFD brokerage that offers a comprehensive range of trading options across forex, futures, commodities, indices, and shares. With more than 10,000 CFD instruments across five platforms, it caters to traders seeking both variety and cost efficiency.

For those starting with a small budget, a minimum deposit of £100 is required to open a standard account.

One of FP Markets’ standout features is its Raw ECN account, which offers spreads as low as 0.0 pips, with a commission of $3 USD per lot per side.

For those preferring a spread-based model without commission, the Standard account starts with spreads from 1.0 pips. Traders can choose from popular platforms such as MetaTrader 4, MetaTrader 5, and IRESS, making it ideal for both beginners and experienced traders.

FP Markets also offers the benefit of FSCS protection, ensuring a level of security for UK-based traders. Although fractional shares are not offered, the platform enables flexible trading strategies with access to a diverse range of global markets. Learn more about FP Markets from our review of the broker.

With a strong Trustpilot rating of 4.8 out of 5 stars based on 9,675 reviews, FP Markets offers a solid foundation for both new and experienced traders seeking competitive pricing and advanced tools. One downside is that it does not offer fractional trading.

5. Trading 212: Share lending, high interest, great for passive investors

The UK-based online trading platform was founded in 2004 in Bulgaria as Avus Capital. It offers a wide range of assets, including more than 12,000 stocks and ETFs.

Other financial vehicles available include exchange-traded commodities, REITs, investment trusts, forex, index futures, commodity futures, and treasury futures. It has more than £25 billion in assets under management (AUM.)

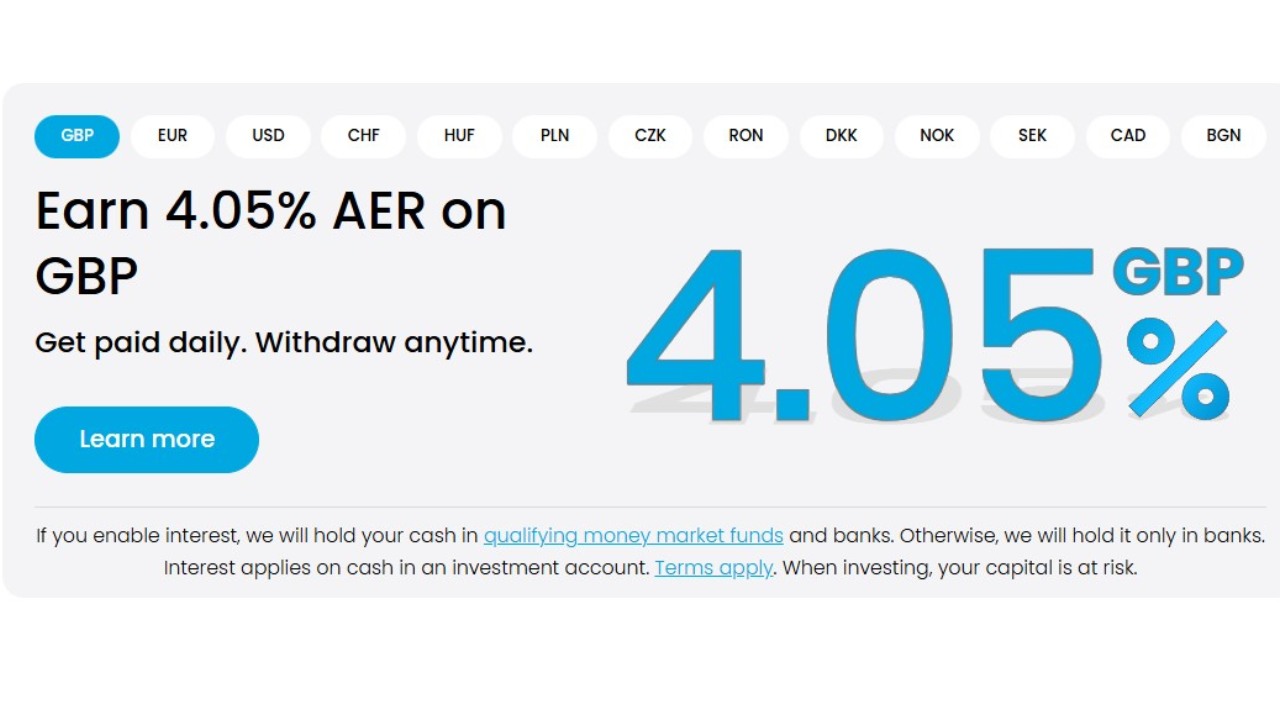

The platform starts with paying 4.05% interest on uninvested funds in your account, so even if you don’t take any action, there are benefits to using Trading 212.

One of the best ways to utilize £100 every month with Trading 212 is to take advantage of its ready-made investment pies, diversified portfolios that automatically invest for you.

You can set your account to automatically send a monthly deposit of £100 into a specific pie, or as little as £1 a month. You are, however, responsible for any rebalancing of the account.

Trading 212 investors can also earn money through its unique share lending program. You retain your shares, but they are lent out to other investors, and Trading 212 receives interest on those shares and passes 50% of it to you.

The interest rate is variable and based on supply and demand. Two big pluses for the platform are that it has a low minimum deposit requirement of £1, and no inactivity fee.

6. IG: Plenty of choices, great for ETF research

The London-based online trading platform began in 1974. While it is known for CFD trading it also provides access to a diverse range of investments, including stocks, shares, ISAs, ETFs, and bonds. Investors can choose from the stocks in more than 13,000 companies, with a significant portion being UK-listed.

If you’re looking to benefit from regular monthly investments of £100, IG offers the opportunity to invest in more than 5,400 ETFs, including an ETF screener that allows you to search for high-performing ETFs categorized by asset class.

It also has what it calls Smart Portfolios, which are managed by BlackRock. They are broadly diversified portfolios with exposure to multiple global markets, including fixed income and equity, as well as alternative investments such as gold and real estate.

The company estimates that, based on an account of £40,000, the annual management costs and other fees would be £288, which is less than what other platforms charge for managed portfolios.

It also offers a range of tax-efficient ISA wrappers and self-invested personal pension (SIPP) options. You can open an ISA by adding an ISA wrapper to a share-dealing account or Smart Portfolio on IG’s platform.

Some of the drawbacks of IG include the minimum deposit requirement of £250 and higher-than-average share CFD trading fees. While it has good educational content, much of it is designed for CFD trading.

7. Saxo Bank: Above-average offerings of stocks, ETFs

The London-based global investment bank, founded in Denmark in 1992, has more than $118 billion in AUM, and a customer base of more than 1.4 million clients. It offers numerous ways to invest £100 a month without overspending. It doesn’t charge a minimum deposit and there’s no inactivity fee.

Saxo offers more than 23,500 stocks to trade from, more than 6,000 mutual funds, more than 5,000 bonds, and more than 7,400 ETFs. It also has an option for stock lending, which is another way to make money off the interest on your stocks that Saxo lends out to other investors.

Its ISAs include more than 11,000 global stocks, ETFs, and bonds. In addition to its extensive product range, the bank provides stock news and educational videos.

Saxo’s fees for ETFs begin at $1 for US-based ETFs and in the UK, it charges a commission of 0.08% (with a minimum of £3) on trades up to £6,000 in value. There’s no minimum deposit requirement.

The company’s interface is easy to use for beginners. Its other fees include a 0.15% custody fee on Classic accounts. It falls to 0.12% on Platinum accounts. and 0.09% on VIP accounts, for investors with a balance of £1,000,000 or more. Another positive is it does not charge an inactivity fee.

8. Freetrade: Intuitive interface, transparent fees

For now, Freetrade, a rival to Robinhood, remains a standalone entity and brand, although it has gained more backing since being acquired by IG this past April. The UK-based investment platform has three tiers: Basic, Standard, and Plus.

Freetrade’s Basic plan doesn’t charge an account fee and is commission-free for trading more than 6,000 global stocks and ETFs. In addition, it allows fractional shares of US stocks and offers a 1% interest rate on up to £1,000 in uninvested cash.

The Standard plan, priced at £4.99, includes more than 6,500 stocks and ETFs, ISA trading, advanced technical analysis, fractional shares on US stocks, plus lower currency conversion fees and pays 3% on uninvested cash. The Plus plan includes all of those options and pays 5% on uninvested cash up to £3,000 and 3.5% above that.

Freetrade’s strengths lie in its simple account setup, intuitive mobile app, and user-friendly interface. It is limited in features compared to other platforms, offering primarily stocks, ETFs, investment trusts, and UK Treasury bills. Investments are restricted to the UK, US, and Europe. It also offers a stocks and shares ISA.

Comparing the top UK brokers to invest regular lump sums with

Breaking down how some of the top UK brokers compare on fees and offerings:

| Platform | Fees for stocks, ETFs | Account minimum | ETFs, stocks available to trade |

| eToro | £0 on stocks and ETFs; spreads on share CFDs | $50 | 700+ ETFs; 6,000+ stocks |

| XTB | £0 for monthly turnover up to €100,000 (after that 0.2% min. €10) | None | 1,800+ ETFs; 6,600+ stocks |

| Admiral Markets | £0 per trade, plus spreads | €250 | 350+ ETFs; 2,900+ stocks |

| FP Markets | Commission varies, typically £3 per side for CFDs | £100 | 10,000+ CFDs including shares, indices, forex, commodities, crypto, and metals |

| Trading 212 | No commission, but spreads apply | £1 | 1,800+ ETFs, 12,000 stocks |

| IG | No commission on direct share trading; Smart Portfolios begin at 0.50% (capped at £250 a year) | None (but £500 for Smart Portfolios) | 5,400+ ETFs, 13,000+ stocks |

| Saxo Bank | ETF trades are a minimum of £3 on trade (up to £6,000 in value) | None | 7,400+ ETFs, 23,500+ stocks |

| Freetrade | Allows commission-free trading on stocks and ETFs | None | 6,500+ stocks and ETFs combined |

Your capital is at risk.

Why commit to investing a set amount regularly?

By regularly investing in the stock market, you can reap significant long-term rewards. Committing to a regular investment amount, like $100 per month, can be a great strategy. This approach, often referred to as dollar-cost averaging, makes investing more accessible and simpler.

Dollar-cost averaging is a strategy that involves investing a fixed amount at regular intervals, regardless of market conditions. It eliminates the need to time the market and ensures you’re buying more shares when prices are low and fewer when they’re high. Over time, dollar-cost averaging helps you average out your purchase price and potentially build a substantial portfolio.

There are several other reasons for investing small amounts regularly, including:

- Reduced risk: By investing consistently, you’re less likely to be heavily impacted by market fluctuations. If the market is down, you’ll be buying more shares at a lower price.

- Improved discipline: Regular investing helps you develop a disciplined approach to saving and investing.

- Take advantage of compounding: Over time, your investments can grow through the power of compound interest. If you invest £100 every month in a UK-based ETF that has historically averaged a 7% annual return, here’s what would happen.

Year 1:

- You invest a total of £1,200 (£100/month).

- Assuming a 7% return, your investment grows to £1,284.

Year 10:

- You’ve invested £12,000 in total.

- Due to compounding, your investment has grown to approximately £16,382.

Year 20:

- You’ve invested £24,000 in total.

- Your investment has grown to approximately £37,407.

The benefits of investing small lump sums

By consistently contributing a set amount, say investing £100 a month to a diversified portfolio, you can:

- Smooth out market fluctuations: Buying more shares when prices are low and fewer when prices are high can help you average down your cost basis.

- Reduce stress: Investing regularly removes the pressure of trying to time the market and can also help you stay focused on your long-term goals.

- Benefit from dollar-cost averaging: This strategy automatically takes advantage of market volatility, potentially leading to higher returns over time.

- Get started saving earlier. Instead of waiting until you feel financially comfortable enough to invest larger sums, micro-investing allows you to start sooner.

The drawbacks of investing regular small amounts

- Investing a lump sum can be risky. If the market drops shortly after your investment, you may be buying at a high price and missing out on potential gains.

- Timing the market is nearly impossible. Even experienced investors struggle to predict when prices will rise or fall.

- Investing small amounts is just a start. To provide enough funds to support you in retirement, it will likely take more than 100 a month.

In summary, regular investing can help you avoid the pitfalls of trying to time the market and stay disciplined in your approach. If nothing else, it helps investors be consistent, and that’s a big part of building long-term wealth.

FAQs on investing small amounts in the UK

What taxes do I pay on my investments in the UK?

What is a stocks and shares ISA?

What platform is the best for regular investing?

Which UK ETF pays the highest dividend?

References

National Study of Millionaires, Ramsey Solutions

Censuswide study on UK investing

BlackRock white paper on investing

Disclaimers and legal information:

eToro is a multi-asset platform which offers both investing in stocks and crypto-assets, as well as trading CFDs.

This communication is intended for information and educational purposes only and should not be considered investment advice or investment recommendation. Past performance is not an indication of future results.

Copy trading does not amount to investment advice. The value of your investments may go up or down. Your capital is at risk.