Robo-advisors in Canada appeared on the investment scene about a decade ago, and since then, more and more investors have warmed to the idea of putting their investments on autopilot. With the adoption of artificial intelligence (AI), robo-advisors are due to become even more sophisticated and popular.

A robo-advisor, or robo, is an online platform that automates the process of investing with the help of computer algorithms. The brokerages that operate these platforms will allocate your funds based on your investment preferences and financial goals that you set when you open an account. Part of the appeal of robo-advisors is that they charge lower fees than traditional financial advisors because they rely on pre-built portfolios, or exchange traded funds (ETFs) that track indices, requiring little human intervention.

Many of us are short on time, and want to save on management fees when investing. In this case, having a portfolio compiled by software based on our needs, level of risk and social consciousness, and then forgetting it, can be quite appealing.

In this guide, we analyzed the nine of the best robo-advisor services available in Canada. Read on to discover our recommendations.

The top Canadian robo-advisor platforms, at a glance

Let’s start with a quick overview of the nine best robo-advisor platforms available in Canada right now. The list will help you choose the one that suits your investing style, experience and funds you have available to invest:

- Wealthsimple: Launched in 2014, it’s an early mover in the Canadian robo-advisor space. The Toronto-based fintech has since added other investment services. It has more than 3 million customers in Canada and more than CAD $38 billion in assets under management (AUM). It’s known for its beginner-friendly platform.

- Questwealth: Known for its low fees, Questwealth is the robo-investing side of discount brokerage Questrade and offers actively managed portfolios of ETFs. Based in North York, Ontario, Questrade has more than CAD $30 billion in AUM. It was founded in 1999.

- XTB: One of the largest contracts for difference (CFDs) and currency traders, XTB, founded in 2004 in Warsaw, Poland, doesn’t provide a traditional robo-advisor service, but it has an Investment Plans feature that includes automatic investments into pre-built portfolios, based on investment goals and risk tolerance.

- RBC InvestEase: The robo-advisor is part of the Royal Bank of Canada (RBC), the largest bank in Canada with more than CAD $1 trillion in AUM. RBC InvestEase offers five types of ETF portfolios, depending on your investment goals and risk tolerance.

- Nest Wealth Direct: Founded in 2014 and based in Toronto, Nest Wealth was one of Canada’s robo-advisor pioneers. It’s now part of the Objectway Group. It has tiered pricing and is popular with larger investors.

- Justwealth: The Toronto company, founded in 2015, offers more than 60 different portfolios, using low-cost ETFs, giving a higher degree of customization compared to some robo-advisors. It has a hybrid model with each investor getting a dedicated personal portfolio manager.

- CI Direct Investing: The company, part of CI Finance, is a leading robo-advisor in Canada with more than CAD $482.2 billion in AUM. It offers an array of investment options, as well as tax-loss harvesting and automatic rebalancing.

- Qtrade Guided Portfolios: The online broker platform QTrade is owned by Aviso Wealth, which is based in Toronto and has more than 500,000 clients and more than CAD $95 billion in AUM. QTrade’s Guided Portfolios use advanced algorithms to build and manage diversified portfolios based on your financial goals, risk tolerance, and investment horizon.

- BMO SmartFolio: The robo-advisor service was launched by the Bank of Montreal (BMO), Canada’s oldest bank, in 2016. It’s managed with assistance from BMO’s full-service investment branch, Nesbitt Burns. It uses five different models, from maximum growth to income, tailored to your goals.

An in-depth look at Canada’s best robo-advisor platforms

Let’s take a more detailed look at the top robo-advisor investing platforms offered to investors based in Canada.

1. Wealthsimple: Best Robo-Advisor for Beginner Investors

The platform has several different options depending on your level of risk, as well as socially responsible investing and a Shariah-compliant ETF. Its socially responsible investing option focuses on the top 25% lowest carbon-emitters in each industry, and every company in its fund has 25%, or at least three women on their board of directors.

There’s no account minimum and it generally has low fees. Wealthsimple’s managed account has a management fee, set at an annual percentage rate of 0.5% for those with less than CAD $100,000 in their accounts. The management fee drops down to 0.4% for those with account balances between CAD $100,000 and CAD $499,999 and for those with balances at CAD $500,000 or above, the management fee falls to 0.2%. So basically, how much you pay depends on the size of your balance. The online app for Wealthsimple Invest is fairly easy to use and allows clients to set up automated deposits, recurring investments and even has a feature that rounds up your credit card purchases up to the nearest dollar, investing the difference automatically in your account. The company pays 4% on uninvested cash balances in your account.

Pros

- Good choice of inexperienced investors

- Low management fees

- Mobile app is easy to use

Cons

- No stock screeners

- Limited educational offerings

2. Questwealth: Hybrid robo-investing for a relatively low cost

Questrade entered the robo-investing market a decade ago and a Questwealth account is a hybrid method of robo-investing because it actively manages its portfolios (instead of just using algorithms), making adjustments as needed. Investors who choose the actively managed service of ETF bundles get free automatic rebalancing of their accounts, automatic dividend reinvestment and if you select it, automatic tax harvesting, where portfolio managers will offset your investment gains with investment losses, so you won’t have to pay as much in taxes.

There are several options of Questwealth portfolios: Questwealth Growth, which is 80% equity investments and 20% fixed income, Questwealth Balanced is 60% equity and 40% fixed income and the Questwealth Aggressive portfolio is 98.5% equities and 1.5% fixed income investments. It also offers Income portfolio and Conservative Income portfolios that have a larger percentage of fixed income investments. Investors can start an account with a minimum investment of CAD $1,000.

For accounts with less than CAD $100,000 The fees are 0.37% of the account (0.25% for a management fee and 0.12% charged by the ETFs held in the portfolio). For those accounts CAD $100,000 or more, the management fees drop down to 0.20%. Questwealth doesn’t have a separate mobile app as it’s part of Questrade’s app.

Pros

- Good customer service

- Solid research tools

- Plenty of portfolio options

Cons

- High mininum investment to start

- Higher fees than some robo-advisors

3. XTB: Solid low-cost choice for experienced investors

XTB is known for its contracts for difference (CFD) trading but coming on the heels of adding fractional trading of stocks, it recently introduced built-in portfolios that are good for experienced investors and have medium- to long-term strategies, though the choices are really up to the individual investors. There’s no commission charge for monthly accounts below €100,000, with a fee of 0.2% after that. The minimum deposit to begin investing is the account currency equivalent of $15.

XTB’s Investment Plans allow investors to have up to 10 portfolios, each with a different strategy, based on selected ETFs. Each portfolio can include a maximum of nine funds. One advantage for Canadian investors is that XTB is available there, unlike in the US. XTB accepts Canadian residents through its French branch.

Some of the options for the Investment Plans include the ability to use recurring payments, also known as auto investing, to supplement each investor’s account. The plans include advanced ETF selection filters so that investors can dovetail their selections with investment goals, along with a risk score feature for ETFs and a performance tab for each. Some of the advantages of XTB is there are no withdrawal fees and it provides interest of 5.2% on cash balances. However, there is an inactivity fee that is the equivalent of €10 a month if there is no activity and no cash deposit within the prior 90 days.

Pros

- Good educational content, including videos

- Low costs for beginning investors

- High interest paid on uninvested balances

Cons

- Limited investment options

- Emphasis is on CFD trading

Disclosure: 75% of retail investor accounts lose money when trading CFDs with this provider.

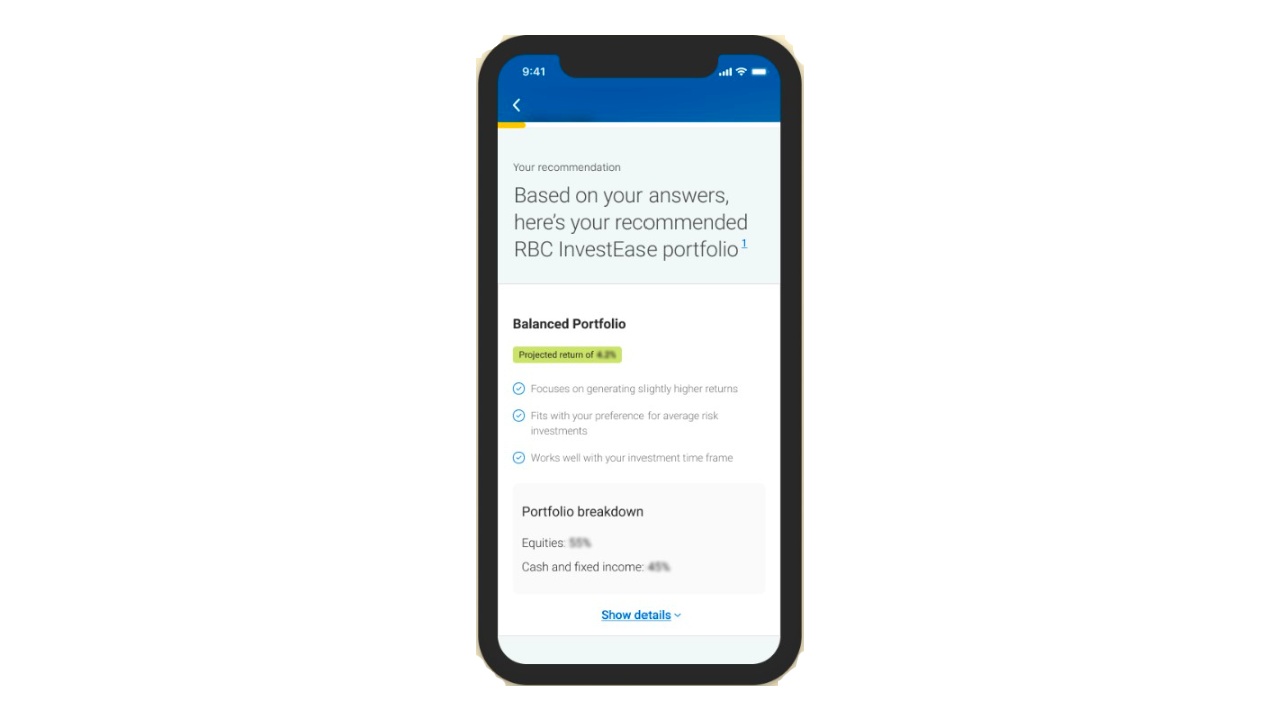

4. RBC InvestEase: Ease of use, more stability with banking giant backing

The size of RBC gives the platform a lot of security, plus for many customers already using RBC for their banking needs, using a InvestEase robo-advisor investment account can simplify things. RBC’s reputation makes it one of the most trusted stock trading platforms. It is free to open an RBC InvestEase account, but there is a minimum CAD $100 to start investing. If you have at least CAD $1,000 in your account, RBC will waive up to CAD $200 of the transfer fees charged by wherever you are transferring your funds from.

RBC InvestEase offers standard managed portfolios, but since it takes ESG investing seriously, there are specific portfolios that target companies with positive environmental and social records. Companies involved with oil, gas, tobacco, civilian firearms, or other controversial products are excluded, but companies focused on renewable energy, social housing, etc., are favoured. It also features a NOMI Insights tool that analyses your other RBC accounts to let you know when and where you have cash that can be invested.

RBC InvestEase suggests portfolios for each investor, based on a series of questions to determine an investor’s priorities. It also provides advisors who are available by phone or email to give professional investment advice. The service charges a 0.5% annual management fee, plus the typical expense ratios that come with various ETFs.

Pros

- Good choice for inexperienced investors

- Plenty of educational resources

- Access to RBC advisors by email or phone

Cons

- Limited robo-advisor portfolios

- No discounts for larger accounts

- No mobile app

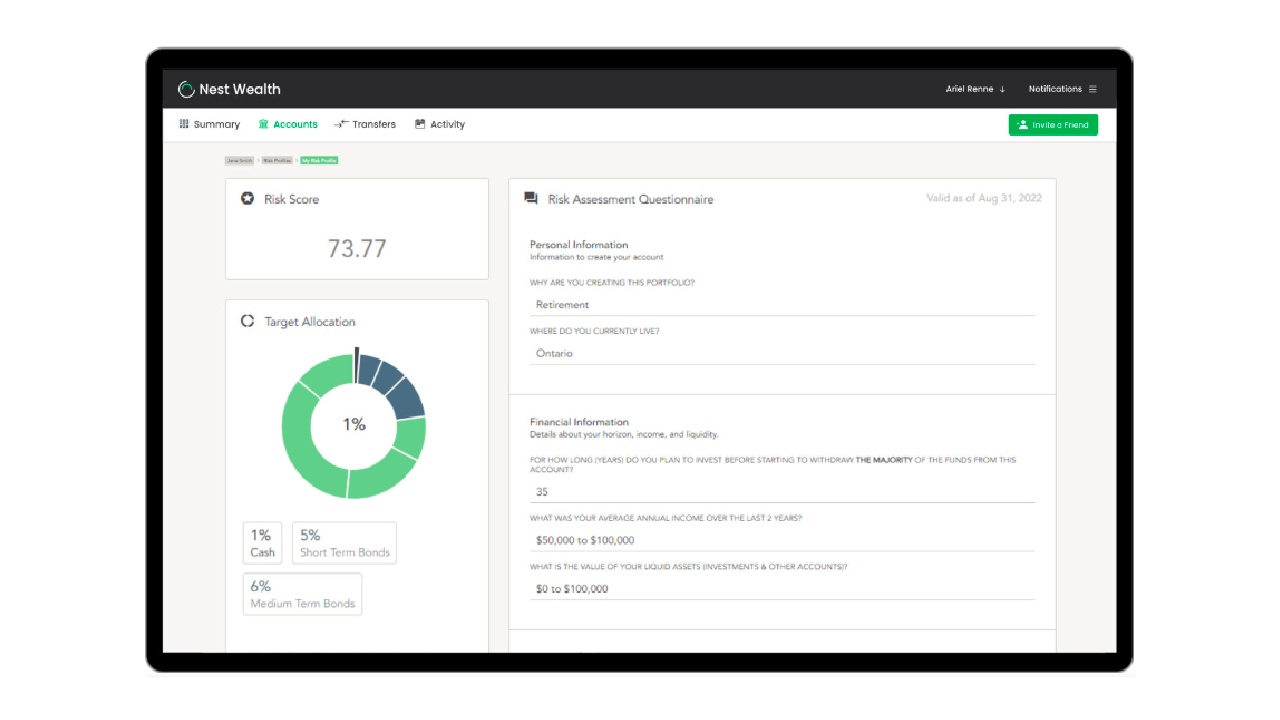

5. NestWealth Direct: Best robo-advisor for larger portfolios

NestWealth was bought out by Objectway Group of Italy earlier this year. While NestWealth is available for individual investors, its robo-advising caters mainly to other advisors and financial institutions.

Its pricing is relatively transparent and its tiered pricing tilts in favour of larger investors, with annual management fees ranging from 0.20% to 0.25%. For example, while accounts under CAD $10,000 pay a minimum of CAD $10 a month, those with more than CAD $350,000 pay CAD $150 a month, a smaller percentage of the account.

A dedicated portfolio manager is assigned to each client prior to their opening an account. Portfolios are monitored daily and automatically rebalanced if they don’t meet certain thresholds. Once you submit your information, NestWealth will review your answers and open an account for you within a couple of business days. A portfolio manager is available to answer any questions by phone, text, or email.

One positive is NestWealth has been using AI for years, not just as a buzzword, but as a way to help advisors show investors who are on the cusp of retiring the best way to utilise their nest eggs and doing so with an individualised approach.

Pros

- No minimum balance requirement

- Good support from portfolio managers

- Individualised approach for investors

Cons

- No tax-loss harvesting

- No built-in socially responsible investing portfolios

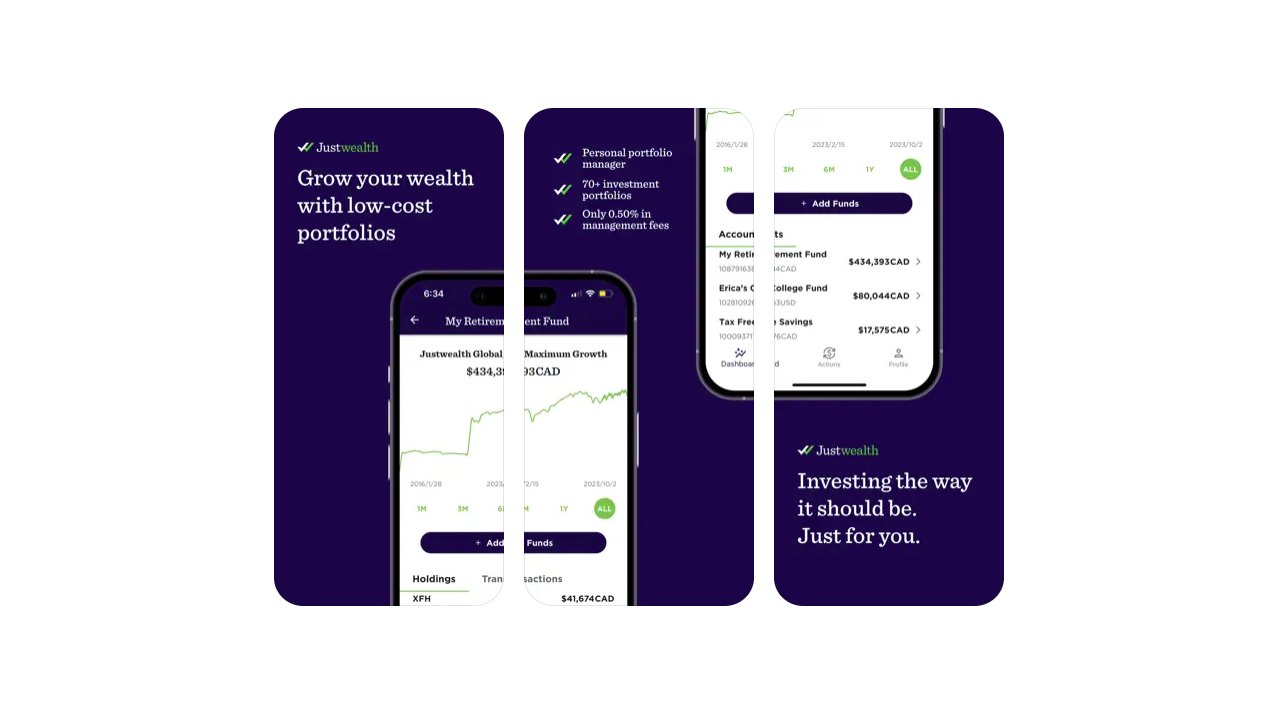

6. Justwealth: Best robo-advisor for plenty of choices

The strength of Justwealth is its huge array of offerings, including 70 different portfolios, based on 42 ETFs from nine different ETF providers. The company also provides a personal advisor for every investor that opens an account.

It offers taxable and non-taxable portfolios in either Canadian or US dollars at no extra cost. A range of income-oriented portfolios is designed to help retirees who may need a fixed income level and don’t want to sell off their securities to provide an income.

It has portfolios for registered retirement savings plans (RRSP), spousal RRSPs, registered educational savings plans (RESPs), locked-in retirement accounts, life income funds, and registered retirement income fund. It also has taxable and non-taxable portfolios in Canadian or US dollars. and a tax-free savings account (TFSA). Its RESP is unique in that it automatically rebalances and matures as the target date for the child’s post-secondary education approaches.

The biggest concern about Justwealth is its fees. Management fees are 0.50% for those with less than CAD $500,000 invested and 0.40% for those with more than CAD $500,000. In addition, there is a 0.20% ETF management fee. If your account has less than CAD $12,000, there is a minimum account fee of CAD $4.99 a month in addition. It also costs CAD $5,000 to open an account, which is higher than most robo-advisors in Canada, though that fee is waived for students, new graduates, and RESP holders.

Pros

- Access to a personal advisor

- Large number of portfolios

- Offers tax-loss harvesting

Cons

- High cost to set up account

- Web site is clunky and no JustWealth mobile app

7. CI Direct Investing: Plenty of options, hybrid model

CI Direct Investing, formerly known as WealthBar, is a subsidiary of CI Financial Group, which has been operating since 1965. The robo-advisor offers a mobile automated investing and saving app. It uses a hybrid model as it offers assistance from licensed financial advisers as well as investment options that are determined by algorithms. Unlike most Canadian robo-advisors, CI Direct Investing is available to Canadian expat investors.

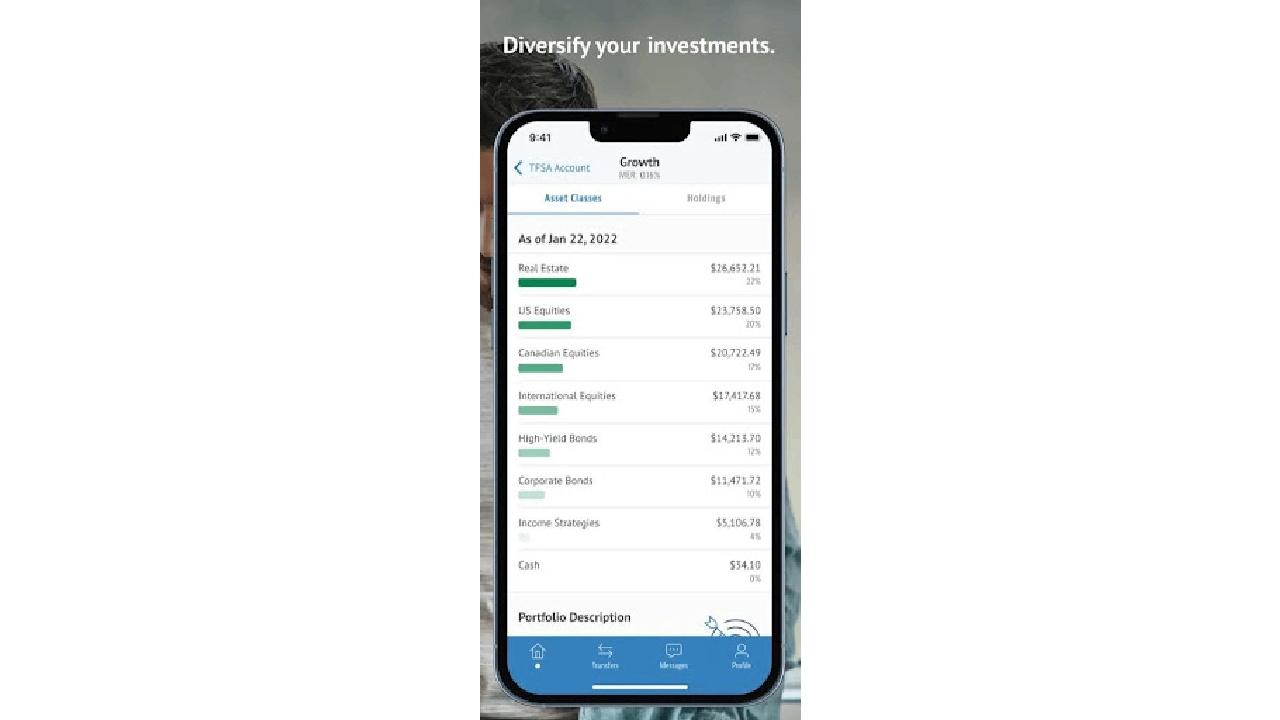

CI Direct Investing offers 11 different ETF portfolios just for passive investing, from an aggressive growth portfolio to an all-equity portfolio and an essential safety portfolio. It also has 15 different socially responsible portfolios, six different active portfolios and a high interest savings portfolio. The platform offers automatic rebalancing as well as tax-loss harvesting

The costs for its accounts are generally low, at least to start. It costs CAD $100 to open an account and investors get their first CAD $10,000 managed for free their first year. After that, though, investors need to invest at least CAD $1,000 in their account and the management fees are slightly above average, from 0.60% annually for the first CAD $150,000 to 0.40% for the next CAD $350,000 and 0.35% annually for accounts with investments above CAD $500,000.

Pros

- Access to human advisors

- Broad swath of portfolios

- Automatic rebalancing and tax-free harvesting

Cons

- Relatively high management fees

- High minimum investment required

8. Qtrade Guided Portfolios: Emphasis on educational resources

QTrade offers investors plenty of educational resources, including reports, ratings, and charts, plus options for support via phone, email or live chat. Its robo-advisor will recommend a portfolio after answering an online questionnaire about financial goals, risk profile, and preferences, then once the account is funded, the Qtrade Guided Portfolios will monitor the portfolio and rebalance it quarterly. Portfolios range from income, to growth and income, to growth, and maximum growth, depending on the asset mix.

Its portfolios are a mix of Canadian, US and global stocks and bonds using low-cost funds. Its choices include a responsible investing option that takes into account companies’ environmental, social, and governance (ESG) performance. Qtrade Guided Portfolios used a sister company, NEI investments, to supply the ETFs for responsible investing portfolios.

While it carries more than 100 commission-free ETFs, QTrade’s management fees were a bit high, starting at 0.60% of your account annually if you hold less than CAD $100,000, dropping down on a scale to 0.35% of your account if you hold more than CAD $1 million. Also, some of the ETFs the company promotes have relatively high fees as well.

Pros

- Plenty of educational resources

- Commission-free ETFs

- Good customer service

Cons

- Inactivity fees

- High management fees

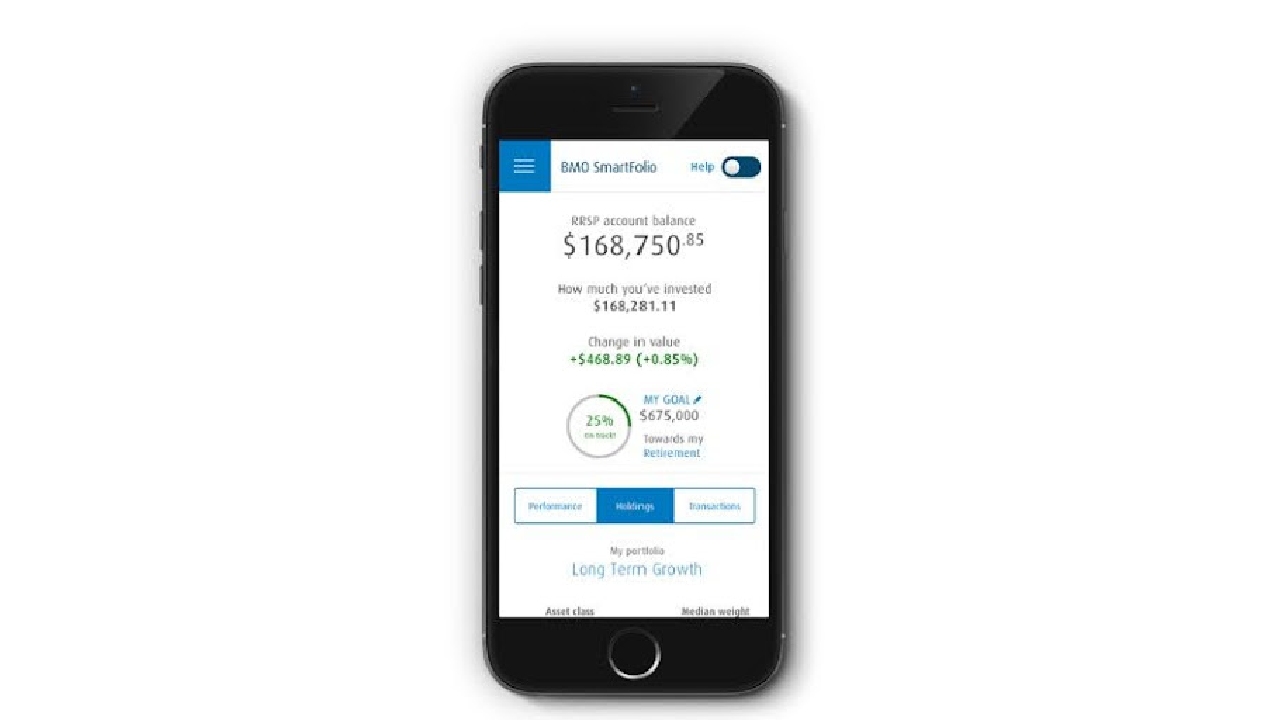

9. BMO SmartFolio: Access to the security and stability of Canada’s oldest bank

BMO is the oldest bank in Canada, so BMO SmartFolio is a good hybrid option for risk-averse investors. The platform is available only to BMO digital banking customers. Investors answer 10 multiple choice investment questions and from that, they are given one of five recommended model ETF portfolios (capital preservation, income, balanced, long-term growth and equity growth).

The portfolios have been developed by five portfolio managers and eight credited financial analysts. The service includes access to financial advisors and they use algorithmic portfolio rebalancing features.

Its management fees vary from 0.40% to 0.70% of your account balance, plus a monthly platform fee of CAD $4 and average ETF fees, and the ETFs are all from BMO. The minimum investment to open the account is CAD $1,000. There are no commission charges.

The biggest issue some have with the platform is the lack of choices as all of the ETFs are created by BMO Global Asset Management.

Pros

- Professional assistance

- Stability, security associated with BMO

Cons

- Lack of ETF choices

- High minimum balance requirement

How do these top Canadian robo-advisors stack up?

| Robo-advisor | Management fees | Minimum needed to begin investing |

| Wealthsimple | From 0.02% to 0.05% | CAD $1 |

| QuestWealth | From 0.20% to 0.25% | CAD $1,000 |

| XTB | No commission for monthly accounts below €100,000 (a fee of 0.2% after that) | US $15 equivalent |

| RBC InvestEase | 0.5% | CAD $100 |

| NestWealth Direct | 0.20% to 0.25% | CAD $1,000 |

| JustWealth | 0.40% to 0.50% | CAD $300 (but CAD $5,000 for all non-RESP/FHSA accounts) |

| CI Direct Investing | 0.35% to 0.60% | CAD $100 |

| Qtrade Guided Portfolios | 0.35% to 0.60% | CAD $2,000 |

| BMO SmartFolio | 0.40% to 0.70% | CAD $1,000 |

Is it worth paying for a robo-advisor?

The answer depends on the level of your investing experience. For beginner investors, it makes sense to use a robo-advisor to reduce risk and increase diversification in your portfolio.

Also, it provides an easy way into investing as you can start with a low initial outlay, and due to the low fees save money on management costs that conventional advisors and portfolio managers would charge.

For investors with more money to allocate and who may wish to be more hands on with their investments other ways of investing may be more suitable that will provide that flexibility in adjusting their portfolios.

That said, robo-advisors are bound to become more popular. According to a report by Grand View Research, the global robo-advisory market size will expand at a compound annual growth rate (CAGR) of 30.5% to $41.83 billion by 2030, from an estimated $6.61 billion in 2023.

How to choose a robo-advisor for your investing profile in Canada

Robo-advisors can be a great way to automate your investments, but choosing the right one is important. Here are five steps to guide you:

1. Define your investment goals and risk tolerance

Before selecting a robo-advisor, clearly outline your financial objectives. Are you saving for retirement, buying a home, or building an emergency fund? Understanding your risk tolerance will help you choose a suitable investment portfolio.

2. Compare fees and costs

Robo-advisors typically charge lower fees than traditional financial advisors. However, it’s essential to compare the fee structures of different platforms. Some charge a flat fee, while others base their fees on your assets under management. Additionally, consider other costs like account minimums and transaction fees.

3. Evaluate investment options and portfolio management

Robo-advisors use algorithms to build and manage investment portfolios. Examine the types of investments offered, such as stocks, bonds, and ETFs. Ensure the platform’s investment philosophy aligns with your goals. Also, consider how frequently the portfolio is rebalanced and if you have control over individual investments.

4. Assess customer service and security

A reliable robo-advisor should provide excellent customer support. Check their availability channels, response times, and reputation for resolving issues. Additionally, prioritize platforms with robust security measures to protect your investments and personal information.

5. Consider additional features and services

Some robo-advisors offer additional features like tax-loss harvesting, retirement planning tools, and access to human financial advisors. Evaluate if these features are valuable to you and if they justify any added costs.

Our methodology of selecting the best robo-advisor services for Canadians

We looked at multiple factors in choosing the best Canadian robo-advisors. The top priority was finding robo-advisors with easy-to-use web sites. After that, we looked for robo-advisors that had low management fees considering what services were available. It was also important to see which platform had solid customer service and good educational resources.

It was also important what investing options were available. While most robo-advisors focus on ETFs, it is important to have plenty of choices within those ETFs. You may want to branch out to other investment vehicles without changing platforms, so we looked for robo-advisors that have other options that may be self-directed as well.

How do we calculate fees per platform?

We checked each brokerage’s web site to determine what fees there may be and then we showed a range of fees, as they often vary depending on how much you have in your account. We also looked at how expensive it was to begin trading with each platform, based on the cost to open an account, and based on the minimum amount it takes to begin investing with the platform.